Key Highlights:

Key Highlights:

-

Q4 2025 shipments down 7% YoY to 34.5 million units

-

Full-year shipments at 154.2 million units, down 1% from 2024

-

Vivo leads with 23% share; Samsung and Oppo follow

-

Inventory overhang and price hikes dampen demand

-

Market shows clear signs of maturation

India’s smartphone market contracted sharply in the fourth quarter of 2025, with shipments declining 7% year-on-year to 34.5 million units, as rising prices and sluggish consumer demand weighed on purchases. Retailers faced mounting inventory pressures, struggling to clear stock amid macroeconomic headwinds that slowed sales momentum.

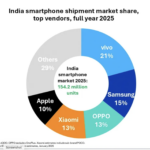

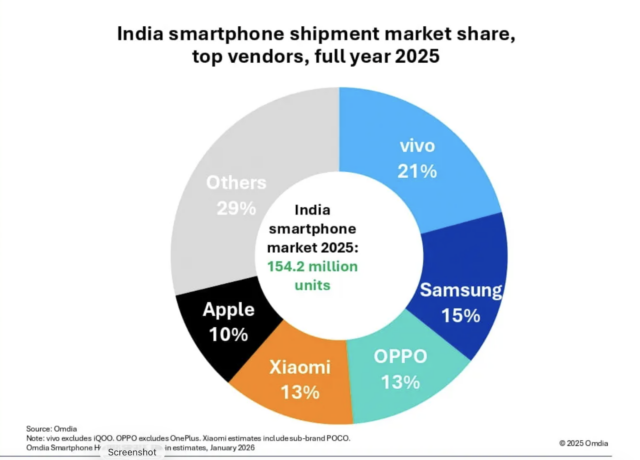

For the full year 2025, total smartphone shipments stood at 154.2 million units, marking a 1% decline from 2024 and signaling clear signs of market maturation after years of rapid growth.

Brand Performance

Vivo emerged as the market leader in Q4 and for the full year, shipping 7.9 million units and capturing a 23% market share. Samsung followed with 4.9 million units (14%).

In a notable shift, Oppo overtook Xiaomi to claim third place, shipping 4.6 million units (13%). Xiaomi and Apple shipped 4.2 million and 3.9 million units, respectively.

Pricing Pressures and Inventory Digest

Rising memory costs and a weakening rupee forced vendors to adjust pricing across both new launches and carry-over models, further impacting affordability. Entering the post-festive quarter with elevated inventories, sales channels remained cautious on fresh stocking. As affordability weakened, sell-out momentum softened from November onward, reinforcing Q4’s role as an inventory digestion quarter.

Overall, the quarter underscored a tougher operating environment for smartphone makers in India, with pricing pressures, cautious channels, and maturing demand shaping near-term prospects.